With Short term Disability ‹ Coverage Payments Will Continue to Age 65 Bus 125

How long does disability insurance last?

Disability insurance is often called disability income insurance – because it actually helps protect your ability to earn income: if you become disabled and are unable to work, it pays a monthly benefit that replaces a portion of your income (typically between 50% and 80%).

The need for disability insurance is real: one in four workers will become disabled during their working years.1 But what counts as a disability? How much do you have to wait until disability benefits begin? And how long will payments last? The answers depend on the type of policy and its specific provisions. This article will help you better understand:

- How a disability policies work

- When benefits should start

- How long benefit payments should last

- How to choose a policy that fits your needs

How disability policies work

There are two main types of policies: Short term disability insurance (or STD) is for temporary disabilities and is designed to provide benefits 3-6 months (and almost never more than a year), or until you can get back to work. Long-term disability insurance (or LTD) is for more severe and even permanent disabilities.

Long term disability insurance is sometimes offered as a workplace benefit, but it can also be purchased as an individual policy. The benefit is designed to last for many years – through retirement if needed – replacing up to 60%-80% of your income if something happens and you can no longer work. Every policy – whether long term or short term, should clearly define these three items:

- The benefit period:The total length of time you can receive benefits. For STD this will typically not be more than a year; for LTD it could range from two years to retirement, or until you recover and are no longer disabled.

- The waiting period:Also called an elimination period, it's the amount of time after you are disabled until you can start receiving benefits. It will generally be shorter for STD and longer for LTD.

- The definition of disability:Every policy has a specific definition of disability insurance stating what is needed to qualify for benefits. A long term disability policy further distinguishes betweenown-occupation disability (you qualify if you can't work in your specialty or field) andany-occupation disability (you only qualify if you cannot work in any occupation for which you are qualified by education, training, and experience. Different levels of disability may also be defined, (for example, "partial disability") which can qualify you for various percentages of your total benefit amount.

STD is typically provided through the workplace, and often as a mandatory, employer-paid benefit with policy options set by the employer. LTD may be more individualized, and choices you make about the benefit and waiting period during the purchase process will determine when payments start, the amount of time they last – and how much your policy will cost. You may also have to decide between an own-occupation and any-occupation definition of disability, because that determines whether you'll qualify for benefits in the first place, and under what conditions.

Two of the biggest myths about disability are that it doesn't happen to younger people and it's largely the result of work-related accidents. Here's the reality:

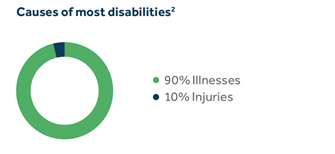

- 90% of all disabilities are caused by illness, while only 10% are the result of accidents.2

- Close to 95% of disabling accidents and illnesses are not work-related. 2

Since disabilities are more common than most people realize, you should think long and hard about whether you'll be satisfied with an any-occupation policy. While the premiums are lower compared to an own-occupation policy, with any-occupation you may not qualify for benefits as long as you can do work.

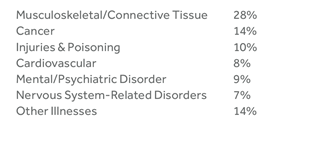

You also need to pay close attention the specific policy provisions regarding specific conditions that are excluded from coverage: nearly 1 in 10 long term disabilities are caused by mental or psychiatric disorders, so make sure these are not excluded by your policy.3

When should disability benefits start?

Whether you have a short-term policy, and long-term policy or both, it's important to know that benefits never start automatically – you have to file a disability claim. The waiting period starts when the claim is filed, so you'll want to do so as soon as possible. For STD plans, the typical waiting period is 14 days – but it can range from 7 to 30 days. Also, STD plans don't make a distinction between an own-occupation or any-occupation disability: the benefit period for an STD plan is typically 3-6 months (and never more than a year) so the assumption is you'll return to your current job or profession when your disability is over.

LTD plans have a much broader range of waiting periods: while 3 to 6 months is typical, some policies will start paying benefits in as little as 30 days – and with others the waiting period can be an entire year. Why such variability? The waiting period can be a lever to help control the cost of their policy. The longer your waiting period, the lower your premiums – so you have to think about how long you could afford to go without an income.

The ideal situation is to have an STD plan benefit period (e.g., 6 months) that matches the waiting period of your LTD plan. That way, there's no lapse in income – when your short-term benefits run out, the long-term benefits kick in. But not everyone has STD coverage. It can be very difficult and expensive to get as an individual, so many sole proprietors and self-employed professionals go without. So, what's the right waiting period for you? Consider:

- Why to choose a shorter waiting period – This will increase your premiums, but if you don't have savings or assets that can cover your expenses without income (and you don't have an STD plan) a short elimination period may be worth your while. But you want to make sure the premiums are affordable, because a lapsed policy will leave you without any protection.

- Why to choose a longer waiting period – If you have an STD policy, a working spouse or savings and assets that can carry you for a while, then an LTD plan with a longer elimination period can lower your premiums – or help make a longer benefit period (below) more affordable.

How long benefit payments should last

People buy LTD policies to replace income for as long as they're disabled, so benefit period length is among the most important decisions to make when applying for a policy. Standard choices include 2, 5, or 10 years; to age 65 and to age 67. A few companies, including Guardian, offer coverage to age 70. While a longer benefit period is clearly desirable, it comes at a cost. How do you make right choice for your needs?

The average duration of a long term disability is 2.5 years2, but remember – that's just an average. Some disabilities are shorter, but many are longer, so a 2-year benefit may not provide the reassurance you're looking for. Even though you have no way of knowing what form your disability will take (if any), from statistical standpoint a 5-year benefit is much more likely to cover your needs. But there are good reasons to opt for an even longer period.

Consider getting benefits to retirement age. The premiums for a policy that provides benefits into or through your 60s may not be much higher than the premiums for a 5-year plan. Why? Insurance companies calculate the risks associated with each policy, and they know they may not have to pay benefits for more than 5 years on most disability claims. So, they can offer a longer benefit period at a relatively low added cost.

Own-occupation LTD coverage through retirement makes particular sense for medical and dental professionals who rely on fine motor skills to practice their craft. For example, a diagnosis of arthritis – or any number of hand conditions – can affect a surgeon's manual dexterity and severely impact his or her ability to earn a living – even though they are otherwise healthy. And any professional with substantial student debt should also consider a longer benefit period in order to help pay it off.

How to choose a disability policy that fits your needs

If your employer offers STD insurance as mandatory or voluntary part of your employee benefit package, that's great – but it's just a start. You should also see if they offer a long term group plan; if you're self-employed you may be able to get coverage through a professional association. Either way, group insurance can be an excellent choice. The company or association is buying for a large group of people, so the premium is typically lower than for an individual policy. In addition, your HR department (or the association's management) will likely have more expertise and leverage to negotiate favorable terms. On the other hand, you'll probably have less opportunity to tailor the policy to your needs, compared to an individual policy. If the premiums are paid with pre-tax dollars (usually the case with employee benefits) then the income benefit you get down the road will typically be taxed. Finally, if you leave the company or association, in most cases you'll also lose your coverage.

Individual long term disability insurance

When you're buying disability insurance for yourself – either as a standalone policy or to supplement group coverage – you have more freedom to tailor it to your needs. As it's (usually) paid for with after-tax dollars, the replacement income it provides is also tax-exempt. It's most often bought through a financial advisor; if you don't have one, or if that person doesn't have much experience with this type of coverage, a Guardian financial professional can give you a disability insurance quote. The cost of an individual LTD policy can vary greatly based on the waiting period and benefit period as well as benefit amount, age, gender, occupation and optional provisions (riders) added to your coverage. You can expect to pay between 1% to 3% of your annual salary.

When you discuss disability plans with your financial professional, be prepared to share as much as you can about your financial situation and goals, so that he or she can tailor your disability policy to your needs. Ask a lot of questions – and make sure you get clear answers:

- How much coverage can I qualify for?

- How does the definition of disability work? Is it own-occupation or any-occupation? What conditions are covered?

- How long will benefits be payable, and when do they begin?

- Could my policy be changed or cancelled — or could my premium increase?

- How do I make a claim if and when needed?

You'll probably want to look at the cost for a few different plan variations before choosing one that provides the best combination of benefits and value for your needs. After you've made a decision, there will be a medical exam and some paperwork to do – and you'll have income protection that can last for years.

Frequently asked questions about collecting disability insurance benefits

Can you collect Social Security disability (SSDI) and long term disability at the same time?

Yes, if you are unable to work you can receive both types of benefits, but you should keep in mind that SSDI is usually much harder to qualify for than a private policy. Most SSDI applicants are actually rejected – and the benefits are typically lower than with a private plan. That's why most experts say you shouldn't rely on SSDI alone for income protection.

What qualifies as a long term disability?

Every policy has its own specific definition of what it means to be disabled in order to qualify for long term disability benefits, but generally speaking there are two types of definitions: Anown-occupation definition means you qualify if you can't work in your specialty or field;any-occupation means you only get benefits if you cannot work in any occupation for which you are qualified by education, training, and experience.

Does long term disability last forever?

No. The benefit period is always limited to a certain number of years which is clearly stated in the policy. Standard choices include 2, 5, or 10 years; to age 65 and to age 67. A few companies, (including Guardian) offer coverage to age 70.

![]()

Get a long term disability insurance quote

Go now

raiwalasputhessir.blogspot.com

Source: https://www.guardianlife.com/disability-insurance/how-long-does-disability-coverage-last